Congress recently passed the One Big Beautiful Bill, and tucked inside is a provision that could make a meaningful difference for retirees. For the 2025–2028 tax years, taxpayers age 65 and older receive a temporary, additional $6,000 standard deduction on top of the regular standard (or itemized) deduction. Some media outlets portrayed this provision as a way to reduce taxes on Social Security. Technically, that isn’t true, but it is an attempt to increase the deduction for those over 65 (many who are taking Social Security) and would reduce their tax bill.

Here are the facts

- Married Filing Jointly (both 65+): Up to an extra $12,000.

- Single (65+): Up to an extra $6,000.

- Income limits:

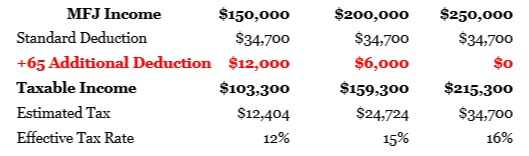

- MFJ: Full benefit up to $150,000 of income; phases out completely at $250,000.

- Single: Full benefit up to $75,000; phases out completely at $175,000.

- Temporary: This is a four-year window (2025–2028) and then it expires unless extended by new legislation.

Quick Example (Illustrative Only)

Couple, both over 65, tax year 2025

Numbers are for illustration; actual results depend on your full situation (credits, other deductions, state taxes, etc.).

How to Think About Roth Conversions in This Window

Above is the easy part. Now for the hard part. What if you have a sizeable IRA and at age 73 will be required to start taking Required Minimum Distributions (RMDs).Those RMDs may put you into a another tax bracket at that time. Does it still make sense to do ROTH Conversions? Should those ROTH conversions be small ones to take advantage of the +65 Deduction or large ones that won’t benefit from the new +65 deduction? Like most financial planning decisions – it depends.

Planning points to weigh:

- Total tax over time: Model your projected taxes over the next 10–15 years, not just this year.

- Don’t forget about IRMAA: Higher income from conversions can raise Medicare Part B & D premiums so it is important to watch this carefully.

- Widows penalty: If a spouse dies what tax bracket will the surviving spouse be in?

- Target tax mix: Decide how much you want in pre-tax vs. Roth for flexibility later.

- Qualified Charitable Distributions (QCDs): If you plan to give from your IRA after age 70½, QCDs avoid taxable income—factor that into conversion amounts.

- Temporary nature: The extra deduction ends after 2028—consider accelerating strategies while it lasts.

If you want to do the easy part, capture the full deduction while you qualify. For the hard math—how much to convert, which brackets to fill, and how this interacts with Social Security, pensions, and investments—contact Oldfather Financial to build a personalized plan for you.