I think parents of Scouts like to see the expressions of co-workers when they asked what they are doing this weekend.

Camping!

So, that is what I did this past weekend. Our Troop along with several other area Boy Scout Troops headed over to Camp Augustine for the annual Klondike Derby. The Troops have sleds (with wheels) that they maneuver around the camp performing various Gold Rush tasks like fire starting, travois building and a compass course while competing against other Troops. They finish off the day with a good old fashioned sled race.

When camping in the winter there is no better time than following the Boy Scout motto of Be Prepared. Having the right gear is essential when you are going to be out in the elements all day and all night. Pro tip: put water into pots the night before so you can heat the water up on the campfire in the morning. The pots will be completely frozen, but will heat quicker than in a plastic jug. The adults get cranky if we don't have any coffee. Just because you are cold doesn’t mean you shouldn’t eat well. We had meals of pancake & sausage, cinnamon rolls, jambalaya, lasagna and even a chocolate chip cookie dessert.

One tradition of our Troop is to track Frost Points. For every degree below 32, a Scout gets a Frost Point. So, on Saturday morning when it was 3 degrees a Scout earned 29 Frost Points. If it had been a balmy 30 degrees, then only 2 points. When a Scout earns 100 Frost Points they are awarded a patch for their uniform. It is their badge of honor that they are a cold weather camper.

So, what does Frost Points have to do with Financial Planning? Scouts actively track their Frost Points to know how many they need for the patch or to brag to another Scout. The first thing they want to know in the morning is how cold it was. I think adults need that same enthusiasm to track their retirement balances and know how they are doing. Instead of just throwing your statement into the file cabinet, look at what your 12/31/19 balance and compare it with your 12/31/18 balance. How much did your portfolio increase last year? 10%, 15%, 20%? It was a great year in both stocks and bonds and your portfolio should reflect it. How much did you contribute to your retirement accounts last year? 5%, 10%, 15% of your salary? Track that also year to year.

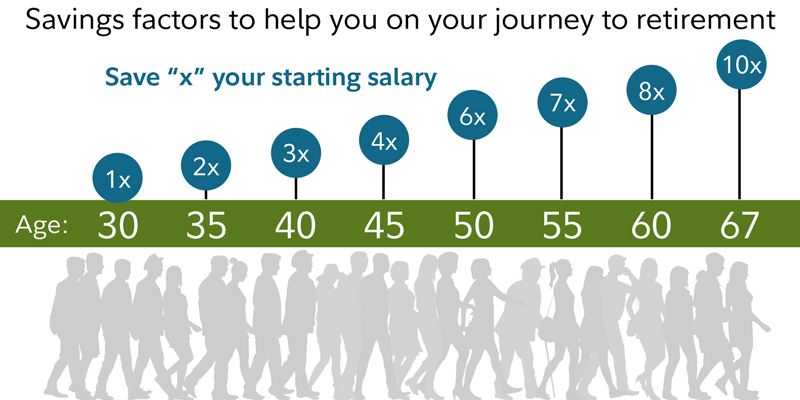

Now look at the simple diagram below from Fidelity to see if you are on track. Find your age and take your salary times the multiplier. Compare that with your retirement account balances. So, if you are 50 years old and make $100,000 a year you should have $600,000 in retirement.

This is only a tool, but it does give you a simple way to gauge how you are doing. If you are below your goal, then start making plans to get back on track before the next time frame. If you want a more detailed analysis of your retirement picture, give Bill or I a call.